For Brian Finn, W’82, 1995 was a big deal. A big, big deal. As co-head of mergers and acquisitions at CS First Boston, Finn helped lead a department that was involved in the execution of more than 100 deals valued at $165 billion. They included Seagrams’ $6.5 billion acquisition of MCA, Union Pacific Corp.’s pending $5 billion acquisition of Southern Pacific Rail Corp. and IBM’s $3.5 billion acquisition of Lotus Development Corp. In all, CS First Boston handled a firm-record 35 transactions in excess of $1 billion each in 1995.

While these and other megadeals — such as The Walt Disney Co.’s $19 billion purchase of Capital Cities/ABC, Inc., Chemical Banking Corp.’s $10 billion acquisition of The Chase Manhattan Corp. and Westinghouse Electric Corp.’s $5.4 billion purchase of CBS Inc. — dominated the news, consolidations were taking place in dizzying numbers among companies large and small.

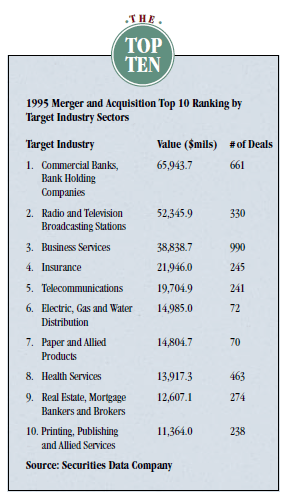

According to the research firm Securities Data Co., global transactions in 1995 came in at a record $866 billion, an increase of 51 percent over 1994’s $572 billion. The United States saw more than 9,000 mergers worth almost $460 billion. That performance smashed 1994’s record year of 7,568 deals valued at $347.5 billion. Even such traditionally low-profile industries as utilities, health care services, and defense were playing “Let’s Make a Deal” at a breakneck pace.

What fueled this merger frenzy? Will 1996 be a repeat? Is there an M&A “Best Practices Guide” to help the more inexperienced players? To find some answers, the Wharton Alumni Magazine recently interviewed several alumni and faculty members who have been involved in various aspects of M & A activity, including investment banking, management consulting, corporate management and academic research.

“Many, many companies find themselves in a position where their business or industry is going global and the competitive dynamics are changing,” says Finn. “And many people have found that another way to increase their growth is through merger and acquisition activity. It’s the old question of buy versus build, and buy has proven to be more appropriate in many industries.”

A good example, says Finn, is Hoechst AG — a major German pharmaceutical company — and its acquisition of Marion Merrell Dow, based in Kansas City, Mo. “If you want to be a worldwide player in the pharmaceutical business,” says Finn, “the conventional wisdom is that you need a substantial stake in the U.S.” At the same time, he adds, many global manufacturers realize that their opportunities for growth lie outside the U.S. As a result, Americans have been buying overseas more than ever.

Even as global competition heats up, many industries — especially commercial banking — are suffering from overcapacity, due in part to technological advances. “Companies are driven to merge principally as a way to cut costs,” says Finn. Chemical and Chase, for example, can now spend “approximately the same amount as one of them would have spent on new technology investment, but spread it over twice the customer base. That creates enormous economies of scale.”

This same phenomenon has occurred in the media and entertainment industry as well, adds Finn, pointing to the economies of scale in content and programming assets created by the merger between Disney and Capital Cities/ABC and the pending Turner/Time-Warner merger.

Nearly as active as the banking and entertainment industries has been health care services. Burdened by cost pressures and overcapacity in many areas, health care was one of the 10 busiest M&A sectors in 1995 (see sidebar). Anheuser-Busch Term Assistant Professor of Management Geoffrey Brooks, who is conducting research on hospital mergers in the San Francisco Bay area, believes that the high volume of M&A activity has its roots in the early ‘80s with the advent of Medicare’s prospective payment system. Under this approach, says Brooks, medical procedures ranging from appendectomies to heart surgery are reimbursed at a standard rate rather than on an individual cost-plus basis.

“It turned around the hospitals’ incentive system,” says Brooks. “Before, the incentives were to build in as much cost as possible, because hospitals were getting profit off the top of whatever they charged. Now, they’re getting a fixed amount. As a consequence, increased cost pressures are necessitating a reduction in lengths of stay as a means of efficiency.” Shorter hospital stays plus an increase in procedures being done on an outpatient basis are resulting in “huge overcapacity in the hospital industry,” he adds.

M&A mania has also been fueled by a raging bull market and favorable interest rates. The Dow, which soared to record levels in 1995, made it easier for companies to finance deals.

“Life feels better when the Dow is at 5000 than when it’s at 3000,” says Finn. “It emboldens people to take risks. Having a highly valued currency, and being able to use equity and do deals in stock,” has been the catalyst for a number of transactions.

“If the stock market is valuing your company at 20 times earnings you can buy a lot more for that stock than when it’s valued at 10 times earnings,” notes Ray Minella, WG’76, managing general partner at Berenson Minella & Co., a private investment and merchant banking firm.

A healthy stock market “also provides a felicitous climate for initial public offerings,” adds Minella, who, prior to co-founding Berenson Minella in October 1990, was a managing director in investment banking at Merrill Lynch and co-head of their merchant banking group.

“The financial entrepreneurs and LBO firms that did leveraged buyouts in the latter part of the ‘80s, who in 1990 were wondering whether they would end up as chumps or heroes, have been able to realize value not by selling the company to somebody else, but by taking it public,” Minella says. The “IPO market of the early ‘90s helped make a lot of firms’ returns look great, enabling them to raise a whole new round of funds.” As a result, he adds, there is about five times more equity capital in leveraged buyout funds now than there was 10 years ago.

THE ‘80s vs. THE ‘90s

While the ‘80s have been described, in so many words, as a hotbed of hostile takeover activity led by a cadre of corporate raiders armed with sophisticated financing techniques, the more recent mergers are perceived as more strategic and better geared to long-term success.

The ‘80s were more exciting than the ‘90s because there were financial players as well as corporate players, says Peter Linneman, Albert Sussman Professor of Real Estate, professor of finance and real estate, and director of the Wharton Real Estate Center. “Largely what you have now is a disproportionate number of corporate players. It’s less exploratory and more professional. And it’s more acceptable because the people making the big offers tend to be the elite of corporate America.”

“When companies announce transactions today, investors look at them nine times out of ten and say, ‘That’s a smart deal,’” comments Finn. “In the ‘80s, buyers were mostly perceived as damaging shareholder value. In fact, most stocks traded down when a company made an acquisition. Not today.”

Another characteristic of the ‘80s, according to Minella, was the ability to achieve great financial returns from an acquisition even when overpaying. Between 1982 and 1987, he says, “interest rates were falling, so the cost of money was always less than was forecast at the time the deal was structured. Also, equity values were rising fast, so that if you bought control of a company and sold off constituent parts, you almost always sold them for more than you thought they were worth when the company was bought. It was not unlike buying wholesale, and selling retail, while the underlying price of assets continued to increase in value. That was the strategy that Kohlberg Kravitz & Roberts (KKR) executed with great success in the Beatrice Foods transaction.” In 1988, Minella adds, “the music finally stopped and those who had come to depend on a rising equity market and lower interest rates were caught short.”

The ease of securing capital in the ‘80s may also have led to misguided merger strategies. “In well-developed markets, people will pursue vertical integration mergers believing that there are great gains,” says Linneman. “In the ‘80s, for example, shopping center owners bought department stores and specialty stores with the rationale that shopping centers need stores, and stores need shopping centers. The shopping center owners thought it was going to be a great strategy and it turned out to be a disaster.”

QUALITY, NOT QUANTITY

Given the mixed record of mergers and acquisitions in the 1980s, some people believe that companies now sense a need to focus on quality more than quantity. “We’re in a period where people realize that they can’t do everything,” says Lawrence Zicklin, WG’59, managing partner and CEO of Neuberger & Berman, an investment banking and securities brokerage company.

“Companies have certain expertise and certain assets. Now they’re trying to rationalize and find out what they can do well and do it, and also determine what they can’t do well and avoid it.” Eastman Kodak Co. and Xerox Corp., for example, recently sold or spun off pieces of their business that simply “didn’t fit,” Zicklin notes.

Harbir Singh, associate professor of management and a leading researcher on mergers and acquisitions, agrees that it is crucial for firms to figure out what types of acquisitions are successful and which aren’t. One way to determine this, he says, is to look at a company’s past track record.

“Study your failed acquisitions and see what you can learn from them,” says Singh. “People very often attribute their failures to poor performance of the acquired firms. But the failure may actually be a firm’s poor judgment in choosing their acquisitions to begin with. Or, it might be incompatibility. Companies should find out whether the key success factors in their current business are applicable to the target firms’ business.”

“We sometimes forget that mergers can be very costly mistakes,” adds Gerald Faulhaber, professor of public policy and management. One particularly spectacular failure was AT&T’s hostile takeover of NCR. At the time of the purchase, Faulhaber says, AT&T had already spent 10 years unsuccessfully attempting to enter the computer business. “So the question is, why would you take a company that’s been a failure in this business and put it together with a company which has been, at best, a modest success?” Faulhaber asks. “All AT&T could do was drag NCR down, which is effectively what they did.”

“We sometimes forget that mergers can be very costly mistakes,” adds Gerald Faulhaber, professor of public policy and management. One particularly spectacular failure was AT&T’s hostile takeover of NCR. At the time of the purchase, Faulhaber says, AT&T had already spent 10 years unsuccessfully attempting to enter the computer business. “So the question is, why would you take a company that’s been a failure in this business and put it together with a company which has been, at best, a modest success?” Faulhaber asks. “All AT&T could do was drag NCR down, which is effectively what they did.”

The fate of AT&T is not that uncommon, according to Daniel Lovallo, assistant professor of management. “When people plan a merger, they tend to take an ‘inside view’ of the problem, which suggests that they will focus on scenarios and develop a ‘future history’ of what will occur. Our research has shown that when you do that, the overwhelming tendency is for people to be overly optimistic.”

Overoptimism may help explain the findings in Singh’s recent study of acquisitions by defense firms. “Most defense firms have been trying to convert their assets and get into new areas,” he notes. “But according to our research, most acquisition cash flows were not impressive. It seems like the defense firms are actually better-off if they stay with their core businesses — even when the business is struggling. The argument is that there are probably profit opportunities within that business itself.”

ADVICE FROM THE FRONT

Michael Bregman, W’75, has been directly involved in a number of transactions, first as chairman and CEO of MMMuffins, Ltd., and currently as chairman and CEO of The Second Cup Ltd., Canada’s leading specialty coffee retailer with more than 500 stores throughout North America and annualized sales exceeding $200 million.

Although MMMUffins’ acquisition of The Second Cup in 1992 was financially successful, the transition phase created some unforeseen difficulties.

For example, as the two companies merged, “what we frequently heard from The Second Cup operators was, ‘We’ve been doing it this way for four years without a problem, so why change now? Why should we throw away coffee after 30 minutes? Why should we throw away the coffee beans after two weeks? Why should we use thermometers to check the temperatures of our lattés — rather than use our hands to feel the outside?’ It was very, very difficult to get some people to buy into the need for an uncompromising approach to quality.”

Pricing and marketing strategies were often contentious, Bregman adds. “If we suggested a certain marketing program, some franchisees would automatically assume that we wanted to build sales so that we could earn more royalties at the expense of their profitability rather than our real goal, which was to help their profitability.”

“We did a lot of things to assist with the transition. For example, we changed the way we bought coffee and certain other supplies and gave the franchisees much more access to purchasing information.” As a result, from the outset, each store saved about $14,000 a year. “And for the first time we allowed the franchise representatives to have a hand in all major decisions that might affect their stores.”

Despite this strategy, he notes, “It took a long time — in some cases three to four years — before franchisees were willing to let down their guard and trust us.”

For those agonizing over the pros and cons of a merger, Bregman says that it is critical to maintain a sense of objectivity and rationality. “People can get emotional and undisciplined in the valuation process. You should never be afraid to say no, or to back away from a deal, no matter how sexy or strategic it looks on the surface. Many times the values are generated by financial engineers who tend to be full of positives and often overlook the unexpected negatives.”

Minella agrees that a lot of “wishful thinking” goes into the M&A process. Completing a deal “is one of the most important things executives are going to do in their corporate life, and it’s much better to make decisions based on realistic expectations than to allow yourself to be sweet-talked and misled.”

Today, Finn says, people are doing smarter deals by pricing and structuring more carefully. And, he adds, “they’re walking away if the deal doesn’t make sense. Mostly, people are buying what they know as opposed to diversifying and creating conglomerates.”

Steve Kaye, WG’90, CEO of GTCO Corp., a privately-owned $10 million manufacturer of digitizers and other computer peripherals based in Columbia, Md., concurs with the “buy what you know strategy.” GTCO, which sells in 45 countries and employs 75 people, recently acquired $2 million Science Accessories Corp., a competing manufacturer of digitizers based in Stratford, Conn.

After reinvigorating GTCO’s operations back in the early ‘90s, Kaye and his management team set their sights on consolidation which they believed would shape their maturing industry in the coming years. Their acquisition of Science Accessories “wasn’t a financial play like the ‘80s where if you could finance it you would do it, even if it didn’t make strategic sense,” Kaye says. “Here, it was two companies in the same business and we could essentially operate both companies off of a single cost structure … Our interest was to drive the industry consolidation and benefit from it as opposed to being subject to it.”

CREATING A COMMON VISION

Once a deal is consummated, the degree to which it is a success or failure depends on how much attention the companies put into cultural integration, says Stephen R. Goldfield, WEMBA’96, vice president and corporate director at Metzler & Associates, a management consulting firm based in Deerfield, Ill.

“With electric utilities, the major functions that the companies perform — such as electricity production, facilities construction, transmission and distribution, and billing systems — are very similar across the industry. So there are not many technical difficulties involved. But the cultures are very different. The companies that do the best job of bringing the merger to a successful completion spend a lot of time pulling the two cultures together.”

In a merger of two midwestern utilities, Goldfield’s consulting firm helped establish transition teams to “create a common vision of what the company wanted to accomplish through its merged operations,” says Goldfield, who specializes in electric utilities. “We had senior management participation from both companies and then created eight to ten task teams to address various issues and functions. It was important that the task teams be well represented by both groups.

“The most critical piece is to merge operations as quickly as possible,” Goldfield adds. “We believe that the uncertainty and the trauma involved for the employees is so great that if you don’t clearly articulate where you’re going, what your vision is, and what your goals are, you will fail. Your people will never recover.”

Bregman concurs on the importance of maintaining open communications with merged workforces. “Often — and I’ve been guilty of this — you spend so much time consummating a transaction, dealing with things like legal and tax issues, that you don’t do justice in spending enough time with the new company,” Bregman says.

He suggests that the process of acquiring another company should include identifying all of the opportunities in which each company would benefit from working together. But “this doesn’t happen by itself. You have to orchestrate an event where the people involved from both organizations can meet face-to-face to jointly solve a problem.”

For example, during The Second Cup’s recent acquisition of U.S.-based Gloria Jeans Gourmet Coffee, The Second Cup was interested in selling one of Gloria Jean’s most popular products — “minicans” of coffee. “On the surface everyone felt that this would be a terrific win-win,” says Bregman. “Our franchisees in Canada were happy to have a new product that would help their Christmas volume, and Gloria Jeans had a new customer.”

Despite the apparent upside, however, Gloria Jeans management viewed their minicans as proprietary and didn’t like the idea that they might be sold in The Second Cup franchises. Bregman’s response was, “If it’s proprietary, isn’t that what we bought? We don’t compete with one another. There are no Second Cup stores where there are Gloria Jeans stores.” The issue was quickly resolved, Bregman adds, but it shows how solid business decisions can be undermined by misunderstandings and lack of communication at the senior management level.

“The way to address these issues is to establish reasons to get together,” he says. “For example, set up a buying committee where representatives from both companies meet to identify areas where they can buy together or buy from one another in a way that helps both organizations … The more at ease employees are with the transition, the more productive they will be.”

Which is not to say that layoffs aren’t a big reality for many employees of merged firms. While numerous managers and investors have reaped huge profits from the M&A wave, thousands of workers have found themselves out of a job. In 1995, layoffs related to corporate marriages accounted for 16.4 percent of the nation’s total job cuts, according to the outplacement firm Challenger, Gray and Christmas.

“I see a lot of this with spin-offs and liquidations,” says Zicklin. “Companies may do this because it is the only way to stay competitive, but I wonder if it’s really good for the country. If shareholders are going to benefit from all of this activity, then what are the employees entitled to? The country is experiencing a reasonable economy and still a lot of people are losing their jobs. If all of these people are truly unnecessary, why did management hire them in the first place? And why isn’t the burden of management error shared more equally?”

Also troubling, says Singh, is the potential to make the wrong cuts. “If you’re going to downsize after the fact, then often the question is, ‘Are you making the right choices?’ You may end up losing the better employees.”

Merger-related downsizing has hit the electric utility industry especially hard, with, on average, about 50 percent of proposed savings coming from the elimination of jobs, says Goldfield.

“If you look at the average personnel reduction as a percent of total employees, companies that merge project somewhere around five to six percent total employment reduction,” he notes. “That’s where the majority of the savings are coming from.” Goldfield says that a recently announced merger between Interstate Power, IES Industries, and Wisconsin Power & Light proclaimed $700 million in costs savings over 10 years, much of that the result of personnel reductions.

THE VALUE OF LEADERSHIP

Transactions are “very much about people,” says Finn. “The interpersonal relationships between and among parties get deals done and kill deals all the time. We can run numbers until we’re blue in the face, and we can conclude that businesses A and B are a compelling combination. But, if the people representing companies A and B don’t want to combine for personal reasons, they won’t be combined.”

Finn says that has led to an acceptance of hostile corporate takeover activity. He points to IBM’s acquisition of Lotus and Wells Fargo’s takeover of First Interstate as examples of strong leadership by Louis Gerstner, chairman and CEO of IBM, and Paul Hazen, chairman and CEO of Wells Fargo. “These were hostile takeovers where the acquiring executive said, ‘I know you don’t want to do a deal, but it’s in my shareholders’ interest, so I’m going to force the issue.’

“The single most important event in recent times,” Finn adds, “was when IBM went after Lotus so quickly and so successfully. It gave a lot of people the backbone to try it as well. It’s not that people wanted to do hostile deals, but that they were willing to go hostile if necessary to accomplish their objectives. … We’re finding that more and more CEOs have the guts to look the public in the eye and say, ‘This is the right thing to do and I’m not going to let one person stand in the way of it.’”

With hostile takeovers completed by companies like General Electric Co., American Home Products Corp., and Johnson & Johnson, “the stigma associated with corporate hostility is gone,” Finn adds.

Goldfield has a slightly different twist on the “people” issue. “The greatest obstacle against a merger taking place in the utilities industry is the management succession issue,” he notes. “It’s widely known in both the investment banking and consulting industry that the best way to identify a merger opportunity isn’t to look at the company’s strengths, weaknesses, overlapping needs or cultures, but to look at the ages of the chief executive officers.”

To effectuate a merger, says Goldfield, “you need one CEO who is close to retirement age so that you have a natural stepdown, and another CEO ready to come in and take over. Lack of management succession planning is the primary reason why negotiations break down.”

LOOKING AHEAD

What lies ahead in the area of mergers and acquisitions clearly differs for different industries. Goldfield, for example, predicts significant change for the traditionally stable electric utilities field. “Historically there has been absolutely no incentive to merge or consolidate,” says Goldfield. “But given certain federal and state regulatory proposals (see sidebar), it is self-evident that competition will be here at some point in time, depending upon whom you talk to and what state they operate in. It’s either two years from now, five years from now, or 10 years from now. It will be here in some form.”

If recent research into San Francisco Bay Area hospitals by Geoffrey Brooks is any indication, the health care services industry should also see increased activity. “In San Francisco, there is an amazing amount of consolidation,” he says. “It’s as if all of the key hospitals in the area are starting to link up. Major hospitals on the West Bay Side are merging with hospitals all the way to Sacramento. It may be in their interest to do this now, but it’s not clear that in the long run the coordination cost is going to be warranted.”

In the health care marketplace of the future — largely driven by managed care — integrated delivery systems will emerge as the winners, adds Kate Flynn, WG’80, vice president of VHA East, a member of a national alliance of not-for-profit hospitals and health care systems. Those winners, says Flynn, will be systems that “can effectively speak for the whole continuum of care, rather than the balkanized, cottage industry we’ve had in the past. The managed care insurers, and now Medicare and Medicaid, are very much driving toward a managed care environment. They will want to deal with large systems that can speak with one voice, that integrate everything: outpatient, doctor’s office, lab, x-ray, hospital, home care, long-term care. That’s what’s leading the drive towards all of this integration.”

Although the conditions that have driven M&A activity over the last two years generally continue to exist, says Finn, “I think 1996 will be a down year from 1995 because 1995 was a hysterical peak. We’re not going to see much activity in the TV network business in 1996, because once ABC, CBS and Turner Broadcasting are gone, how many network TV transactions can there be? Many industries are done. They’ve evolved. The hospital industry had a huge wave of activity a year and a half ago and that’s probably pretty much over. The railroad industry has had a wave of activity but I’m not so sure it’s over. The banking industry has had a wave of activity that is definitely not over. So each of these industries has its own cycle going on.”

Finn cautions, however, that a stock market crash could slow down activity substantially, as could the inability of the government to nail down a budget agreement. Other potential barriers: a material economic shift in Europe or Asia or an interest rate spike. These factors make M&A activity “vulnerable to change in a negative direction,” says Finn. “But from where we sit today, I would forecast that ‘96 will be a very active year. Perhaps the second most active year in history.”

![]()

![]()

Although not as glamorous as telecommunications and entertainment, the utilities industry was among the busiest in terms of mergers in ‘95 with 72 deals valued at $15 billion, according to Securities Data Co. That performance also placed utilities as the sixth most active sector in ‘95, a major leap from a 17th place rank in ‘94 with total deals valued at just under $7 billion.

A catalyst for these mergers, says Stephen R. Goldfield, WEMBA’96, vice president and corporate director at Metzler & Associates, a management consulting firm based in Deerfield, Ill., was the passage of the Energy Policy Act in 1992 which “created a competitive wholesale power market.” In addition, Goldfield says that in 1994, California started a regulatory proceeding aimed at evaluating the opportunities for having open retail competition within the state. This action would allow industrial and commercial customers to actually choose their energy suppliers, similar to how customers can now choose their long distance carriers.

“Just the mere investigation of that possibility caught the interest of many other states and started a groundswell feeling in the industry that companies — sooner or later — were going to have to compete,” says Goldfield.

As a result, utility companies have been seeking ways to cut costs and increase their competitive position. A natural reaction, says Goldfield, “is to grow bigger to achieve some economies, eliminate some redundant operations, and merge.” At the same time, he adds, there has been some loosening of other regulations, including a public utilities holding company act that prohibited electric utilities that also owned a gas utility franchise from ever buying another utility out of state. This type of restriction is now being relaxed.

The increased competition will also create the need for beefed up marketing efforts, says Goldfield. A number of people from outside the industry have moved into leadership positions at major utilities, he adds, especially executive-level marketing posts which are being increasingly filled by individuals from consumer products companies.

“There will be a few more dynamics in the industry from a financial performance perspective, but I don’t think it has the growth prospects that will make it a darling industry of Wall Street. You’ll see the betas of stocks going up, the investor return requirements increasing over time, the probability of more bankruptcies and greater earnings fluctuations. But electric energy growth has really flattened out in this country and it’s not likely to increase.”

In the traditionally conservative utilities industry, Goldfield cites one company that has been successful by taking an aggressive merger approach. Entergy, an electric utility based in New Orleans, acquired operations that gave them a strong presence in Louisiana, Arkansas, Mississippi and parts of Texas.

“Entergy invested heavily in integration of those companies and in the pulling together of the overall operations,” says Goldfield. “At the same time, Entergy distinguished itself by also investing heavily in nonregulated business activities as a diversification strategy that centered on different business lines. For example, they are heavily invested in energy management services across the U.S. So while they cannot sell electricity outside their franchise service territory, they can sell services.”

Eager to compete in a deregulated environment, U.S. utilities have been among the more active players in seeking overseas partners. The U.K. has opened up its electric utility system to competition, and many of the distribution companies have actually been acquired by U.S. electric utilities in the past 12 months, says Goldfield.

The U.S. industry is looking to the British model to see if it’s working. U.S. utilities are also snapping up many Australian distribution companies. Because these overseas electric companies are subject to competition, U.S. utilities, Goldfield adds, are hoping to learn how to operate more competitively in the deregulated environment of the future.