In the past couple of years, a new breed of pharmaceutical companies such as Valeant, Turing Pharmaceuticals, Questcor, and Sodelis, among others, has entered the U.S. drug market with aggressive pricing strategies for certain drugs that are intended to maximize shareholder profits. Critics of these strategies say that they disproportionately favor the company’s bottom line over patients’ needs, and now their profitability may be in jeopardy thanks to the power of public backlash. Some examples of drug prices that have sparked outrage:

- Questcor bought the rights to Acthar Gel, which treats infantile spasms, a rare form of childhood epilepsy. Questcor raised the price of a vial from $40 to $23,000.

- Valeant bought heart drug Isuprel and raised the price of a single vial from $440 to $2,700.

- Valeant bought diabetes drug Glumetza and raised the price from $800 for a 90-day supply to over $10,000.

- Valeant raised the price of Edecrin (a diuretic) from $470 in 2014 to $4,600 in 2015.

- Turing Pharmaceuticals increased the price of Daraprim (treats life-threatening parasitic infection) from $13.50 a tablet to $750.

- Rodelis Therapeutics raised the price of a drug to treat multidrug-resistant tuberculosis from $500 to over $10,000 for the same number of pills.

- Mylan doubled the price of its famous and unanimous drug EpiPen.

How did prices get so high?

In the United States, drug prices are not regulated by any federal government agency. Other than generic medications, which face a lot of competition, prices for brand name drugs and specialty drugs are often set by how much the market will bear. For instance, in the case of drugs used to treat and cure Hepatitis C (i.e., Sovaldi, Harvoni), the cost of these medications easily tops $150,000 per treatment. The price justification for these medications is two-fold: 1) Recoup research and development investments (with the U.S. being the backbone of R&D returns for the world); and 2) Set drug prices at a value point below the ultimate cost of forgoing treatment. (Undergoing a liver transplant due to a case of untreated Hepatitis C can cost upwards of $750,000.) It’s estimated that by 2020, pharmacy costs will account for 31 percent of overall health care costs, becoming the number one driver of client expenses.

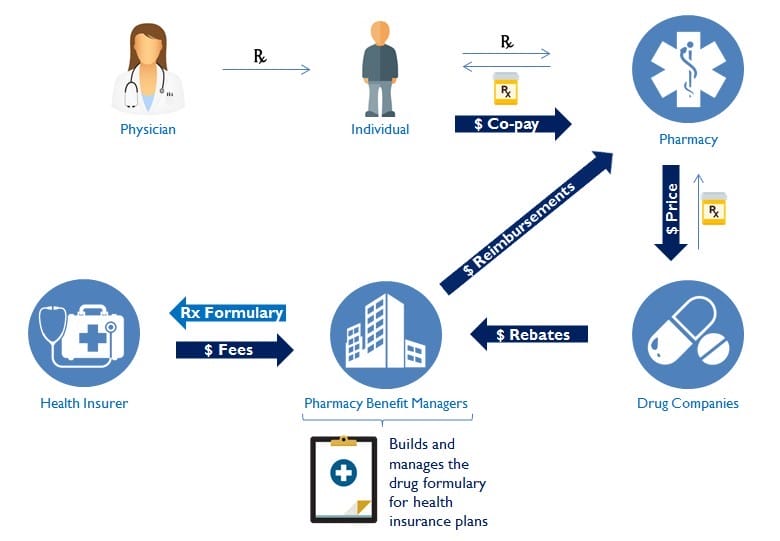

Another factor that impacts the cost of drugs is the role played by pharmacy benefit managers (aka PBMs). Created to increase efficiency and reduce costs by acting as third-party administrators of prescription drug programs for commercial health plans, PBMs now control prescription drug benefits for more than 260 million Americans, with three companies—Express Scripts, CVS Caremark, and OptumRx, controlling almost 80 percent of the market. PBMs contract with drug manufacturers and pharmacies in an effort to develop and maintain the drug formulary used by healthcare plans. They earn revenue by negotiating discounts and rebates with drug manufacturers, charging various fees to pharmacies (including fees in order for pharmacies to have the right to be compensated by the PBM), and processing and paying prescription drug claims fees to health insurers.

Illustration by: Cassia Peralta

The role of PBMs in the health care industry is complicated and opaque, leading to potential conflicts between the financial interests of PBMs and the best clinical outcomes for the consumers of medication. There is evidence that PBMs can price drugs arbitrarily, which adds a level of unpredictability to pharmacies and makes it more difficult to serve beneficiaries.

After years of amassing record profits, in part due to unjustifiable fees and considerable market consolidations, PBMs are also coming under heightened public and congressional scrutiny.

An End to Overpricing

While there are no bills expected to pass in Congress that would punish companies for jacking up the price of drugs, there are other non-legislative factors that are beginning to threaten the profitability of this strategy. Now any company making moves in this direction faces a backlash from consumers, negative press, political outrage, SEC investigations, and amped up press coverage of alternative drugs as a result. Case in point: Mylan doubled the price of their EpiPen without reasonable justification and had to endure a media spectacle because of it. Whilst this profit-seeking strategy seems to have worked in the short-term, the countervailing costs of such measures do not seem to be paying off over the long-term.

Public outrage not only seems to encourage competitors to rush their cheaper Rx versions (generic substitutes or generic equivalents) to the market as fast as possible; it also makes consumers turn away from the medication whose prices were abused. Mylan introduced a generic version of EpiPen for half the price in order to properly compete with two other generic epinephrine auto-injectors that came into the market in February 2017. It remains to be seen if the public relations damage of Mylan’s move will be temporary or long-lasting.

Other blue chip pharmaceuticals such as Pfizer, Merck, Novartis, and Johnson & Johnson have used this moment to come out and say that they are capping the price increases of their drugs, and that the aforementioned price abuses in this report are the works of a few bad actors. Their mission is to bring life-saving medications to the market and charge a fair price that will bring returns for their investments, but won’t maximize short-term profits at the expense of healthcare consumers, plan sponsors, taxpayers, and Medicare.

PBMs have also moved quickly and aggressively to keep these overpriced drugs off of their clients’ standard formulary, limiting their availability to consumers. By doing so, PBM clients are ensuring that their patients receive the more affordable generic formulation of specific medications. Branded drugs, such as Glumetza, when excluded will not be processed, even at retail pharmacies that have signed agreements with Valeant to prioritize the dispensing of Glumetza.

Valeant seems to be the poster child for what can go wrong with this myopic profit- maximization strategy. Their stock is at record lows due to heavy debt load and declining revenues. The CEO was replaced. Competitors moved in quickly to capitalize on the prescription price arbitrage. Consumers were spooked and sought cheaper alternatives, most likely making a permanent switch away from Valeant.

Political outrage not only brought the pharma and PBM industries under the microscope. It also sparked serious discourse about the long-term viability and solvency of the U.S. health care system and what future alternatives might have to be considered. As is, this runaway freight-train that is our health care system is headed for difficult times ahead, made worse by an aging demographic, soaring healthcare cost and medical inflation in general.

The merit of this profit-seeking strategy does seem to have run its course. In the end, this aggressive revenue approach created an arms race for profit among a new breed of pharmaceuticals and drove up the cost of healthcare spending for everyone in the U.S. Given that health care spending is already more than one-fifth of the U.S. economy and larger than the entire GDP of France, nonstop exploitation of this system by these price-hike strategies could have detrimental long-term effects to the health care delivery model in the U.S. These short-term early profit wins could ultimately turn out to be a pyrrhic victory for the players in question and the industry as a whole.

Editor’s Note: This post was co-authored by Marcelo Wright, a health insurance officer in Washington, D.C.