In my first part of this blog series, I discussed how Tier 2 suppliers, if leveraged properly, could be a catalyst for increasing supplier diversity. My thoughts on this topic have been shaped over decades of working in the supplier diversity arena.

Businesses owned by women and minorities represent more than 50 percent of all U.S. businesses, but only generate 6 percent of the revenue. An expansion from traditional Tier 2 to multitier reporting could be a strong driver of growth for supplier diversity across corporate America.

My curiosity led me to several questions regarding the Tier 2 programs of the best-in-class companies. As I began to analyze some of the aggregate results of these programs, I wondered what would happen if the companies at the top of the food chain expanded the requirements of their Tier 2 programs.

Many of these programs already contractually require reporting participation from the top portion of their supply base, anywhere from 50 to well over 500 prime suppliers (either Tier 1 or a direct contractor to the buying organization). These Tier 2 spend reporting requirements also include specific diversity spend goals. However, in our experience most programs stop at Tier 2 reporting.

The Network Effect of Multitier Reporting

I decided to explore the possibilities for economic impact in a corporate supply chain that required multitier diversity spend reporting. That is, reporting down to Tier 5 of the supply chain.

To provide a realistic illustration, I used data representing average benchmarks across multiple companies. Since Tier 2 requirements and policies vary across organizations, I used common requirements that have been incorporated in the key assumptions below:

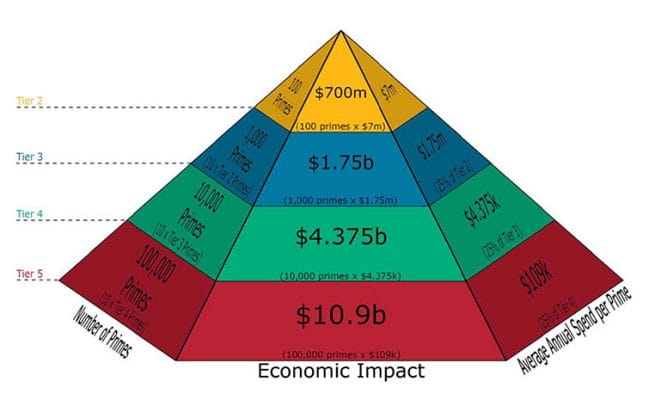

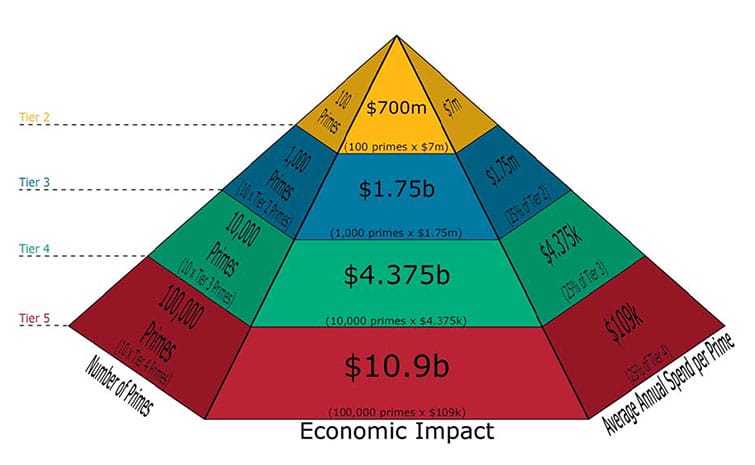

• Contractually require top 100 prime suppliers to report diverse spend quarterly (Tier 2).

• 10 percent annual subcontracting goal (direct + indirect)

This is where reporting typically stops, but to illustrate the impact of required reporting down to Tier 5, we went further. What if each tier of primes below Tier 2 required reporting from their top 10 primes?

Spend assumptions are as follows:

• Average annual Tier 2 spend = $7 million

• Average annual Tier 3 spend = $1.8 million (~25% of Tier 2)

• Average annual Tier 4 spend = $438,000 (~25% of Tier 3)

• Average annual Tier 5 spend = $109,000 (~25% of Tier 4)

As noted in the diagram above, expansion beyond the traditional Tier 2 (yellow) creates a massive economic impact. In this example, pushing reporting requirements down to the Tier 5 level results in a total economic impact of nearly $18 billion (sum of Tier 1:Tier 5). This represents an increase of 25 times the impact of Tier 2 alone.

When organizations spend significant dollars with small businesses in local markets, this often leads to relatively significant revenue growth for that business. This, in turn, leads to job creation and positive impact in local markets like community development. It’s hard to ignore the other benefits, such as increased supply market competition, innovation, enhanced quality and lower costs. The same would not occur if organizations award business back to a larger, older, less innovative incumbent supplier.

Back in the early 2000s when I was chief procurement officer of a major corporation with responsibility for supplier diversity, our manual data collection processes using Excel spreadsheets made it impossible to even think of such a strategy. However, the scalable technology and tools available make it extremely simple and inexpensive to build a truly world class program that delivers real quantifiable results. A win-win for all.