The Wharton School began in 1881, but Wharton’s Jeremy Siegel began even earlier. When researching his 1994 bestseller, Stocks for the Long Run, Siegel uncovered stock performance data stretching back all the way to 1802, revealing that stocks have outperformed every other investment class by a considerable margin. This once-surprising truth is now nearly universally accepted—a sign of his wide influence.

This long view of financial history makes Siegel, the Russell E. Palmer Professor of Finance, an ideal commentator on market performance during Wharton’s anniversary year. An icon at Wharton and a guru of equity investing, Professor Siegel looks ahead at how the Age Wave will affect the future for investors, workers, and global economies.

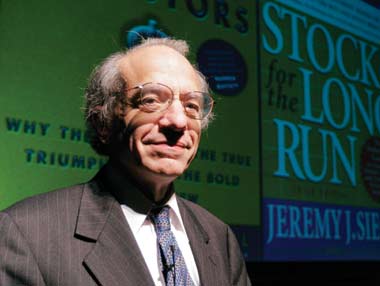

Published in 1994, Stocks for the Long Run catapulted Wharton Professor Jeremy J. Siegel from an esoteric economist to a wizard of finance. And it ushered in six years of the greatest boom market in history.

Siegel’s latest book, The Future for Investors, stemmed from two questions audiences persistently asked him on the lecture circuit. Investors were sold on the notion that stocks were the best bet for the long run, but wanted guidance on which stocks. And with 77 million baby boomers eyeing retirement, investors were fretting over the impact on the financial markets as they aged.

As Siegel researched the answers, he found a crucial link between the two seemingly-disparate topics. With the help of his research assistant Jeremy Schwartz, another book was born.

Like Stocks for the Long Run, The Future for Investors began with an astonishing lesson from history. From 1871 to 2003, reinvested dividends accounted for 97 percent of the real return of stocks. Capital gains contributed just 3 percent. Siegel then applied that lesson to a future in which the aging population will be, as he puts it, “the most critical long-term economic issue facing the developed world.”

While analyzing stock performance for The Future for Investors, Siegel received a phone call from Jonathan Steinberg, W’88. He wanted to create an index weighted by dividends rather than market capitalization, and hoped Siegel would help test the data.

Siegel went beyond testing the data. He joined Steinberg’s company, Wisdom Tree Investments, as a senior adviser. This year, at age 60, after nearly 35 years of teaching and with more 300,000 copies sold of one of the most influential investment texts of all time, he took for the first time—and passed—his Series 7 and Series 63 exams.

Wharton Alumni Magazine sat down with the Siegel in his home overlooking the Atlantic Ocean in Longport, NJ, to discuss the importance of history, his latest work, and the opportunities and challenges facing investors ahead.

In your new book, you conclude that growth does not guarantee returns. Why not?

It’s a surprising result. When you look at the S&P 500 since its inception, you see how much its sector weights have changed over time. Information technology, health care and financials were only six percent of the index in 1957 and they’re 50 percent of the index today. Materials and energy were 50 percent then. They’re only 12 percent today.

If you bought the original S&P 500 stocks, and held them until today—simple buy and hold, reinvesting dividends—you outpaced the S&P 500 index itself, which adds about 20 new stocks every year and has added almost 1,000 new stocks since its inception in 1957.

Over the past 50 years, information technology and financials were just mediocre in terms of their performance. Energy, which has contracted, has outperformed. I’ve done the analysis and it turns out less than one-third of a sector’s return is due to its expansion or contraction. In other words, less than one- third of the return is explained by growth. The rest is the price you pay and the dividend you receive. That’s pretty amazing.

The problem is new firms are overvalued when they’re put in the index. People get excited about new stocks. People rush to buy them for their portfolios. And they pay too much.

Why does the aging of the population have such significant implications for global trade?

Throughout history, the old have sold to the young, and the young work for the old and provide them goods. In the U.S., life expectancy has gone up while the retirement age has gone down. The difference between life expectancy and retirement age used to be 1.6 years in 1950. Now it’s 14.4 years. That’s a huge difference.

Meanwhile, the number of workers per employee in the U.S. has gone down dramatically, from 50 in 1950 heading toward 2.5 in 2050. In Japan, the largest population by age group in 2050 will be 75 to 80 years old. And the number of workers per retiree goes down to almost one for one.

So the biggest questions facing the developed world are, who’s going to produce the goods, and who’s going to buy the assets?

If there are not enough people producing goods and generating income, they’re not going to be able to purchase the assets. We’re going to have to work much longer, and the retirement age will go from 62 today to 73 or 74. It even goes up more than life expectancy, and so for the first time in history that gap will shrink, from 14.4 years to 9.2 years.

Now I ask myself, are there any solutions?

Faster productivity growth is one. But if I plug into my model 3.5 percent productivity growth—that’s 70 percent above the long term average of 2.2 percent—I find it only buys a little bit. And the reason is, wages are tied to productivity and benefits are tied to those, so it doesn’t produce a lot of margin.

Then I look at immigration and one model says we can still retire at 62 if we bring in half a billion people over the next 45 years. That’s twice the population. I’m a liberal on immigration, but that’s a lot of people.

But if I look at India, and I look at the dynamic of its age profile, the number of workers per retiree does go down but it stays high during this critical time of our baby boomers retiring. What I see happening in the world is that the older, developed countries are going to sell their assets, and the buyers are going to be developing countries.

The answer to our questions, who will produce our goods and who will buy our assets, is the same. It’s the developing countries.

How large a swing in economic prowess between developed and developing countries do you envision?

I do a projection of stock market capitalization, which is now overwhelmingly in the developed world, close to 92 percent. By 2050 I think only one-third of the stock market capitalization will be in the developed world. Two-thirds will be in the rest.

It’s inevitable. By the middle of this century developing countries will own most of the world’s capital. They will have controlling interest in most of the world.

It comes back to demographics. The developed world is currently 15.2 percent of the world’s population. But the developed world today produces 56 percent of the world’s GDP. By 2050, the population of the developed world will shrink to 11.8 percent.

What does that mean? I put some productivity growth figures on various countries and I predict that by 2050 what we call the developed world today will only produce 23 percent, and the developing world 77 percent of the world’s GDP.

Let’s break that down even further. I think by 2050 the U.S. will contribute 11 percent of the world’s GDP, Western Europe six percent, Japan two percent and Canada one percent. The sum of those is 20, which is the same as China.

By 2050 China will be 20 percent, and India 16 percent, of the world’s GDP. And that’s based on conservative projections. I wouldn’t be surprised if India and China were even further ahead.

But actually, I think it’s the best solution to a lot of our problems—Social Security, Medicare, the baby boomers retiring, what’s going to happen to their assets. We need to make this trade. If I put it into my global model, this trade that takes place between assets and goods, I can get us retiring not at 62 but only at 67, which is still very reasonable.

This trade is just a global extension of a trade made through history, which is the old selling to the young and the young providing goods to the elderly.

So what are your thoughts on the U.S. trade deficit?

In that context the trade deficit is not worrisome. Of course I’d like it to be a little less now, but I believe we will have a trade deficit for the next 30 or 40 years. I think Europe will. I think Japan might. This is a lot to think about. It has tremendous implications. But it’s vital. It’s critically important.

The growth of the developing world is not just good for them. It’s not just charity. Yes, we want the poor to not be poor. But it’s also critical to us that the poor not be poor.

The workers and the goods the developing world provide actually prevent a much poorer future for developed countries if they relied instead on their own populations.

If we just had to rely on our own people, we would have to retire that much later, or we would retire earlier but poorer. And the markets would go down. People think they have wealth, but without the developing countries there are not enough buyers out there.

My feeling is the stock market will hold up, if we open markets to the buyers from Asia and the rest of the developing world. It’s going to be really critical in terms of producing good returns in the future. That’s why when I see developments like CNOOC and Dubai Ports World, I become very worried. If that protectionism becomes entrenched we would see a much poorer future.

Protectionism seems to be fueled in part by anxiety. What is society’s responsibility to those who have lost their jobs to global trade?

As you go through this analysis, you see that globalization is just so important. All these Age Wave problems don’t completely disappear, but they are ameliorated to a huge extent by a global outlook and the trade that can take place. Nothing that I see that the developed world can do by itself would come close to solving the problem.

If we want public policy to buy globalization, we must address the issue of who’s going to be the loser from globalization. There’s no question that for unskilled labor, their relative wages are going down because two billion workers from China and India are suddenly hitting. That’s supply and demand. But the gains we’re making from that trade are more than enough to provide these people with whatever support and income substitution they may need. One thing we learn from economics is you can have a win-win situation. It’s not just zero-sum. The winners can win enough that they can, in fact, compensate the losers for their losses.

But it has to be done carefully. All the studies that have been done so far on protecting jobs show the costs are many times the salaries of the people whose jobs are actually saved. The loss to the consumer of protecting 100 workers in, say, a chemical plant, costs consumers a thousand workers’ worth in income. That just doesn’t make sense, from an economist’s standpoint.

Can we compensate the workers who have lost? Yes we can. There’s enough gain here for everybody to be winners. We have to develop ways to transfer some of the profits and higher incomes that globalization implies to compensate people who lose from globalization. It is much better to do it that way than to restrict globalization, because then everyone loses.

You’ve said that the developing world can be the saving grace for the developed world’s upcoming demographic tidal wave. How does that translate into opportunity for investors?

Don’t just jump into the fast growing markets. Look at China. It has had more than 9 percent real GDP growth but it is at the very bottom in terms of returns. There’s actually a slight negative correlation between GDP growth and return, for the same reason it exists in stocks.

Too many of the fast growing countries get over-bid. They get over-priced. But if you find an established company with a strong international brand, then you have a reasonably priced investment that takes advantage of the changing world economy.

What made you decide to take your first major role in a company after more than 30 years teaching and doing research?

I was very upset about the rollercoaster that cap-weighted indices took in the bubble. Weighting stocks by fundamentals attracted me as an alternative to capital-weighted indices. When Jonathan [Steinberg] called me and said he was developing a dividend-weighted fundamental, I thought, ¡®This is really good for investors.’ I think this is a better way to index. My feeling is I’ll be helping investors if I help develop some sort of vehicle that will give them better returns.

I did the research, with my research assistant Jeremy Schwartz, and it was extraordinary. Going back through history, whether looking at it by sector, large-cap, small-cap, it’s all there. It corresponds to what I found on dividends in the book.

What has been a defining development in the financial markets over the past half century that will continue to shape the world over the next 50 years?

It depends on how broadly you define it. I think we ended the 20th century with the knowledge that democratic market- oriented systems, for all their failings, are the best way to deliver the good life to people. We’ve experimented with communism, fascism, socialism. We’ve seen that can’t be done. We have more commonality now on an outlook of how we should run the system.

I think mankind is naturally competitive. What we have to do is funnel the competition in a way that helps society. I think there’s recognition that we want freedom of markets, but we need to have a social fabric. There needs to be recognition of income disparities. There are real reasons why some people fall behind. And a society that doesn’t take cognizance of that will also suffer, and may not survive.

And that is very important looking ahead to globalization. You must take care of the losers, but my feeling is the winners will have sufficient resources to do it. It has to be presented as a package that can benefit all. We have to think ahead about that if we want globalization. Once we can benefit everyone, people will see globalization’s potential and hopefully grasp it as the goal that can realize most of their dreams.

Ritu Kalra, W’96, a frequent contributor to Wharton Alumni Magazine, is a freelance business writer.

SERENDIPITY AND THE ACADEMIC LIFE:

The Story Behind a Bestseller

Serendipity is the invisible hand that has guided Wharton Professor Jeremy Siegel throughout his life. A math major at Columbia University, he happened upon an economics class during his junior year and two weeks later declared he had discovered his life’s work.

Economics, not capital markets theory, took Siegel in 1967 to Massachusetts Institute of Technology, where he struck a lifelong friendship with fellow doctoral student Robert Shiller while the two were standing in line for mandatory chest x-rays. It was as an economist that he taught at the University of Chicago from 1972 to 1976, where he was guided by giants such as Milton Friedman. (Friedman, it turns out, was awarded the Nobel Prize the same day Siegel was supposed to go on a blind date set up by the then-president of the Federal Reserve of Philadelphia. Siegel was so eager to get back to Chicago to celebrate his friend’s achievement that he left a barely intelligible message canceling the date, nearly derailing the relationship with his wife before it even began.) Even the invitation to teach at Wharton rested squarely on his macroeconomic credentials.

Investments didn’t come into the picture until 1989, nearly two decades into Siegel’s career. The topic may not have come up at all had it not been for a phone call from a colleague. The New York Stock Exchange had asked fellow Wharton finance professor Marshall E. Blume to write a history for the institution’s then-upcoming 200th anniversary. Blume asked Siegel to collaborate on the project.

An astute student of history, Siegel suggested to Blume that they expand their focus on the 200 years of the New York Stock Exchange’s institutional history to include two centuries of stock returns as well. When he finished analyzing the data, Siegel was stunned by the now-familiar results: Since 1802 (the earliest year for which numbers were available), stocks had returned between 6.5 and 7 percent with considerable consistency, rewarding investors with higher returns and less volatility than any other asset class. The persistency of stocks, now dubbed “Siegel’s Constant,” had never been explored in such depth before.

This was trail-blazing work. But Siegel’s research was too vast for a history on the New York Stock Exchange, and the institution rejected it.

Ironically, it was Shiller—whose Irrational Exuberance later warned of the danger of stocks in March 2000—who encouraged Siegel to turn his research into its own book. Blume was supportive as well.

Siegel heeded the advice, and the result was Stocks for the Long Run.

“Had Marshall [Blume] never called me about that project, would I have done the book? Who knows,” says Siegel. “It was all in me, but nothing had ever sparked me until that.”