Thought

![]() “You want to ask the crowd for two bits of information—not just for their own answer, but also for their predictions about the answers of other people in the crowd.”

“You want to ask the crowd for two bits of information—not just for their own answer, but also for their predictions about the answers of other people in the crowd.”

How much should businesses trust crowdsourced data? In “A Solution to the Single-Question Crowd Wisdom Problem,” researchers including Wharton marketing professor John McCoy propose a method for crowdsourcing that can help generate better, more accurate results: Weigh these two responses, and rely on the “surprisingly popular” answer.

Data Interpreted

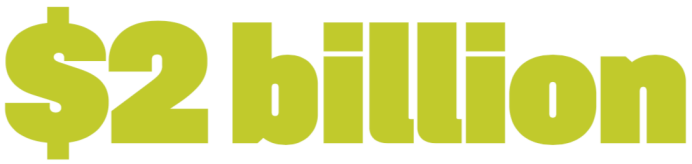

Approximate amount raised in 2015 through charitable promotions run by North American businesses

Such initiatives yielded just $100 million in 1990. In the paper “Philanthropic Campaigns and Customer Behavior: Field Experiments on an Online Taxi Booking Platform,” researchers including Wharton vice dean for global initiatives Serguei Netessine find that although charitable giving through business promotions is on the rise, it doesn’t lead to long-term customer loyalty.

Data Interpreted

The United Nations warns rising temperatures should be contained to this amount above pre-industrial levels to avert severe impacts of global warming.

Knowledge@Wharton recently invited three experts—including Eric Orts, Wharton faculty director for the Initiative for Global Environmental Leadership—to analyze the outcome of the 24th annual Conference of the Parties, a U.N. climate change meeting of nearly 200 countries.

Thought

Fintech Finds “Invisible Prime” Borrowers

For decades, the main recourse for cash-strapped Americans with less-than-stellar credit has been the payday loan and its kin, which charge interest rates in the triple digits. But a slew of fintech lenders is changing the game by using artificial intelligence and machine learning to sift out true deadbeats and fraudsters from “invisible prime” borrowers—those who are new to credit, have little credit history, or are temporarily going through hard times but are likely to repay their debts.

The market fintech lenders are targeting is huge. According to credit scoring firm FICO, 79 million Americans have credit scores of 680 or below, which is considered subprime. That number doesn’t include another 53 million U.S. adults who don’t have enough credit history to even get a credit score.

“The U.S. is now a non-prime nation defined by lack of savings and income volatility,” said Ken Rees, founder and CEO of fintech lender Elevate, during a panel discussion at “Fintech and the New Financial Landscape,” a conference recently held by the Federal Reserve Bank of Philadelphia. According to Rees, banks have pulled back from serving this group, especially after the Great Recession. “Prime customers are easy to serve,” he noted, since they have deep credit histories and a record of repaying their debts. But there are folks who may be near-prime but are just experiencing temporary difficulties or haven’t had an opportunity to establish credit histories. “Our challenge … is to try to figure out a way to sort through these customers and figure out how to use the data to serve them better.” That’s where AI and alternative data come in.

To find these invisible primes, fintech startups use the latest technologies to gather and analyze information about a borrower that traditional banks or credit bureaus don’t use. The goal is to consider this alternative data and more fully flesh out the profile of borrowers to see who’s a good risk. “While they lack traditional credit data, they have plenty of other financial information” that could help predict the ability of such would-be borrowers to repay a loan, said Jason Gross, co-founder and CEO of Petal, a fintech lender. What, exactly, falls under “alternative data”? Jeff Meiler, CEO of fintech lender Marlette Funding, cited such information as a person’s assets, net worth, cars, utility payments, schooling, and occupation.

Data Interpreted

Full-time employees in the U.S. who are female

Women make up nearly half of the American workforce, yet they aren’t represented proportionally among leadership and across industries. Panelists discussed why it is imperative for women to have a bigger voice in the capital markets at a recent conference hosted by Knowledge@Wharton and Impact Investment Exchange, an organization founded by Durreen Shahnaz WG95.

Thought

“It’s not a marathon; it’s a series of sprints. To perform at your best in every sprint, you need time to recover. To be your best as a leader, you need time to recharge.”

Wharton Dean Geoffrey Garrett turned three leadership clichés on their heads for the latest Wharton CEO Academy, an executive-level event in New York. Garrett suggested replacing “Stick to your guns” with Kenny Rogers’s “Know when to hold ’em, know when to fold ’em” and advised attendees to “question everything”—but not always aloud.

Published as “K@W Data” in the Spring/Summer 2019 issue of Wharton Magazine.